| Bank of England policymakers voted to keep interest rates at 3.75%, opting for caution due to the unpredictability of the Middle East | The UK faces a weaker economic outlook than any other G7 nation as a result of conflict, says the International Monetary Fund (IMF) | Office for National Statistics figures indicate a more encouraging picture for the UK economy than expected |

Bank of England holds rates as inflation complicates outlook

On 30 April, Bank of England (BoE) policymakers voted to keep interest rates at 3.75%, opting for caution in the face of a rapidly changing inflation picture driven primarily by ongoing conflict in the Middle East.

As the price of Brent Crude oil reached a four-year high, the BoE’s Monetary Policy Committee (MPC) voted eight to one to keep Bank Rate on hold, with the majority of committee members opting for a wait-and-see approach to the unfolding energy shock. The decision, which was widely anticipated by markets and economists, came just days after the release of the first official inflation figures from the Office for National Statistics (ONS) since the war began.

ONS data confirmed that Consumer Price Index (CPI) inflation rose to 3.3% in the 12 months to March 2026, up from 3.0% in February, with motor fuels making the largest upward contribution to the monthly change. Services inflation also ticked higher, reaching 4.5% in March, while core CPI inflation, which strips out energy, food, alcohol and tobacco, eased marginally to 3.1% from 3.2%.

The inflation data reinforced the case for keeping rates on hold. All 62 economists polled by Reuters in the week before the MPC meeting expected rates to remain unchanged, with a cut considered unlikely given the ongoing global volatility.

After announcing the decision, BoE Governor Andrew Bailey stressed that keeping rates unchanged was “reasonable… given the situation of the economy and the unpredictability of events in the Middle East.” He also signalled that the BoE would act “forcefully” to control inflation and may choose to raise rates if the energy shock persists. He added, “Whatever happens, our job is to make sure that inflation gets back to the 2% target after the initial impact of the war on energy prices has passed.”

UK braced for biggest growth hit of major economies

The UK faces a weaker economic outlook than any other G7 nation as a result of the conflict in the Middle East, according to the International Monetary Fund (IMF).

April’s World Economic Outlook warned ‘the global economy is threatened with being thrown off course’ due to the US-Israeli war with Iran, causing the IMF to revise its global growth forecast for 2026 to 3.1%. This is down from 3.3% forecast in January, before the hostilities began.

The IMF’s baseline projection assumes a limited and short-lived conflict, but it suggested a longer or broader conflict could significantly weaken growth and destabilise financial markets. In a severe scenario, global growth could fall to just 2%, a level reached on only four occasions since 1980, including the Global Financial Crisis and the Covid-19 pandemic. However, the IMF advised central banks to resist the temptation of raising interest rates to counter rising inflation, noting, ‘Reacting strongly to flexible commodity prices, when supply constraints are present only in the related sectors, brings down inflation fast but risks a recession later.

The IMF now projects UK GDP growth of 0.8% in 2026, down from a previous forecast of 1.3%, the largest downgrade of any G7 economy. This is due to the UK’s heavier reliance on imported gas and relatively low gas reserves compared to other European countries. It also cited weak economic momentum in the second half of 2025 as a compounding factor. The IMF expects UK inflation to average 3.2% across 2026, up sharply from the previous forecast of 2.5%, with the IMF projecting inflation will near 4% before easing back to the 2% target by the end of 2027.

Markets

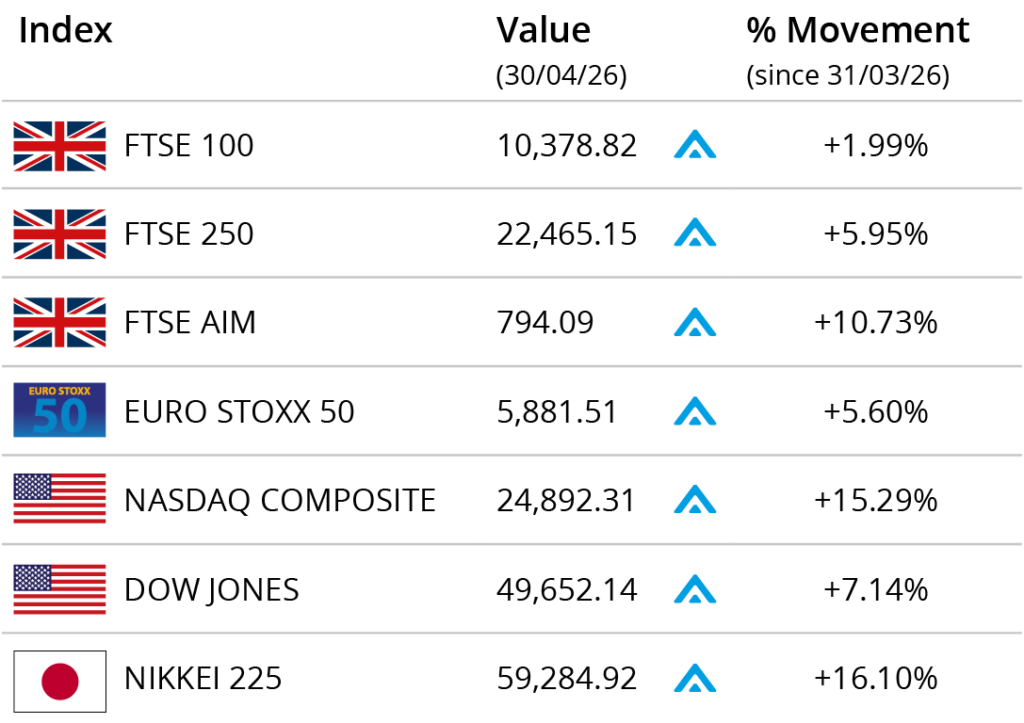

Major global markets largely closed the month in positive territory. In the UK, the FTSE 100 made strong gains on the last trading day of the month as investors processed an array of earnings data, the MPC rate decision and the latest developments in the Middle East.

The blue-chip index closed April almost 2% higher on 10,378.82 and the mid-cap focused FTSE 250 ended the month nearly 6% higher on 22,465.15. The FTSE AIM registered a gain of over 10% in the month to close on 794.09. The Euro Stoxx 50 closed April 5.60% higher on 5,881.51. In Japan, the Nikkei 225 closed the month on 59,284.92, gaining over 16% in April. In the US, the Dow Jones closed April up over 7% on 49,652.14. The NASDAQ recorded a monthly gain of over 15% to close on 24,892.31.

Oil prices remained volatile throughout the month. Prices surged in the final days, briefly reaching their highest level since 2022, after President Trump stated that the US would maintain its naval blockade of Iranian ports, signalling the possibility of renewed military action should negotiations falter. Despite the late-month rally, prices eased slightly by month-end, with Brent Crude closing at around $110 per barrel, recording a monthly gain of nearly 6%.

On 28 April, the United Arab Emirates announced its intention to withdraw from the Organization of the Petroleum Exporting Countries (OPEC), effective 1 May. The unexpected move comes after the UAE was the target of drone and missile attacks by fellow OPEC member Iran.

On the foreign exchanges, the euro closed the month at €1.15 against sterling. The US dollar closed at $1.36 against sterling and at $1.17 against the euro.

Gold closed April trading around $4,635 a troy ounce, a loss of around 1.38% in the month.

UK retail sales rebound, but consumer confidence weakens

The latest retail sales data from ONS painted a more encouraging picture for the UK economy than expected, but consumer confidence remains fragile.

Total retail sales volumes rose 0.7% in March, reversing February’s 0.6% fall and well ahead of forecasts of a 0.1% decline. The primary driver was a sharp spike in fuel purchases, which jumped 6.1%, the highest monthly reading since April 2021, as motorists filled their tanks following ongoing conflict in the Middle East. Clothing and technology retail also posted solid gains, although food sales fell 0.8% for the month.

However, GfK’s long-running Consumer Confidence Index fell four points to -25 in April, its lowest reading since February 2023, and the third consecutive monthly decline. The Savings Index was the only measure to improve, rising five points to 32. This indicator typically reflects households building contingency funds rather than optimism about the outlook. Indeed, consumer expectations of the UK economy over the next 12 months slid six points to -43.

Neil Bellamy, Consumer Insights Director at GfK, said, “Consumers really do have the jitters now.… Consumer confidence is deteriorating sharply, with fuel prices and threats of more energy price increases acting as constant reminders of inflation.”

UK jobs market clouded by uncertainty

While official labour market data appears stable, geopolitical pressures have added uncertainty to a cautious hiring environment.

Figures released in April showed the unemployment rate was 4.9% in the three months to February 2026, despite expectations it would remain at 5.2%. This decline can be partly attributed to ”fewer students seeking work alongside their studies,” according to the Director of Economic Studies at ONS, Liz McKeown.

Meanwhile, the number of job vacancies fell by 29,000 in January to March 2026, reaching 711,000, the lowest level since the period February to April 2021. Meanwhile, the number of payrolled employees fell by 74,000 in the year to February 2026, with an early estimate for March showing a further monthly decline of 11,000 to 30.3 million.

Analysts noted that while the headline unemployment figure was not alarming, the direction of travel in vacancies and payrolled employment is harder to dismiss.

Domestic policy is also a contributing factor. The first wave of Employment Rights Act reforms took effect in April 2026, introducing new day-one rights on sick pay, paternity leave and bereavement, changes that, combined with previous National Insurance increases, have added to the cost and complexity of hiring for many businesses.

All details are correct at the time of writing (01 May 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.